Pershing conference takeaways and how to justify your fees as a wealth management adviser

/Change challenges every industry and technology seems to be the key disruption factor across every industry from retail, fast food/restaurants, to financial services. The truth of the matter is that technology has always been a disruption. Did you know, Proctor and Gamble ("P&G") use to be the leading manufacturer of candles? However with the introduction of kerosene around the civil war, the new format or "technology" forced P&G to move onward and by happen chance entered the soap business. Today, these innovations take the form of automation. We see innovation around robotics (physical) and robos (software) everywhere, even McDonald's. You might soon see these at higher value restaurants.

See here (video about a restaurant with a robotic kitchen): https://mashable.com/2018/05/08/four-mit-graduates-have-opened-a-restaurant-where-robotic-kitchen-prepares-the-meals/#PM8ZFuTb4Pq9

Within our segment, wealth management, robo-advisers are creating pricing pressure on RIAs, challenging the "value proposition". Nonetheless, I hardly believe that Robo's will upend and destroy the livelihoods of financial advisers just as much as I do not see automated restaurants become the end of chefs. Technology is but a means to an end, and since the dawn of time, technology has advanced humanity because of the leaders that leverage technology to further the business model (purpose).

Coming from Pershing INSITE (AppCrown was a Gold Sponsor), we've learned much from Lisa Dolly (Pershing CEO) and where the organization is heading. Pershing is looking to leverage technology to become an enabler for financial advisers to grow/build a better business. The conference highlighted:

- Focus on technology to change how engagement happens after the client meeting; operations, integrations and better collaboration with the custodian platform.

- Using technology to create better business models - Pershing actually discussed Salesforce.com and their new account opening solution they're looking to deploy to advisers.

With robo's offering 25 basis points providing what is essentially a modeled portfolio, RIA's will need to defend their value proposition going forward. Perhaps the future is to go up market (in terms of service and value)?

Let's consider the value proposition and why Robo's are attractive:

- Ease of use - a "think less" approach.

- Quick and dirty - the concept that the liability falls on the software and less work required from the individual.

- Tax savings and long term benefits - that's certainly the selling point from Wealthfront.

For the RIA, technology needs to be seen as a great tool rather than a "be all solution" that will help the wealth management firm overcome value proposition challenges. Here are some ways to accomplish this:

- Create a unique mobile experience for your clients by changing how your firm interacts with younger generations (and I mean Generation X, those in their mid 40's that is using mobile and inheriting money from the baby boomers).

- Create an automated new account opening process that streamlines the client engagement and onboarding process. Make it simple, seamless and sophisticated (3 S's).

- RIA's ought to consider incorporating greater value into their firm's service beyond financial planning and investment management (and seek to charge more). Since most RIA's are outsourcing their investing work through TAMPs, it makes more sense for financial advisers to add more services to their clients such as:

- Net Worth tracking and assumptions of economic risks that affect liquidity requirements for retirement

- Estimated true net worth liability tracking - track liabilities that affect an individuals net worth based on healthcare, estate/wealth transfer taxes, and beneficiary risks

- Portfolio optimization risk analysis - how optimized or "optimal" are your clients portfolio given their age and retirement requirements?

- Service Tip: Consider adding comprehensive tax planning, estate and trusts planning to enhance the value of your firm beyond purely planning. Consider what technology could automate, enhance and go up market in what your firm can provide to the client. This, in turn, ought to provide a basis for increased fees. If we consider the following demographic change, we see how much education and services to hedge the risks of transferring wealth can become an "in demand" service within the next 5 years.

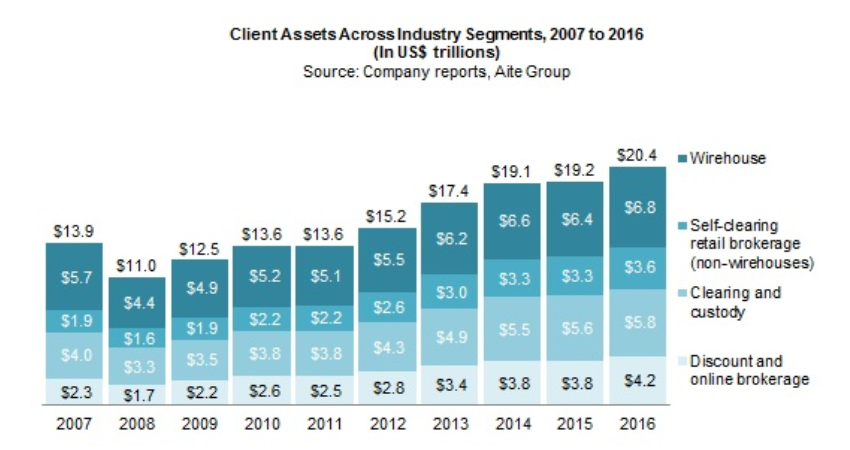

If we look at historical information, the reality is that robos are attacking a very small % of the wealth management pie (trillions vs billions). Independent financial advisers should focus less on the fear of "robos", because that's what the press wants - they all need a villain to sell viewership - consider where technology fits within your wealth management organization and focus on truly making a difference in your operations through integrations.

If you can spare some time, let's schedule a discussion about your wealth management firm and our technology solution: https://my.timetrade.com/book/5MHHL