Money At Risk: Wealth Management firms might soon lose and fight harder for assets

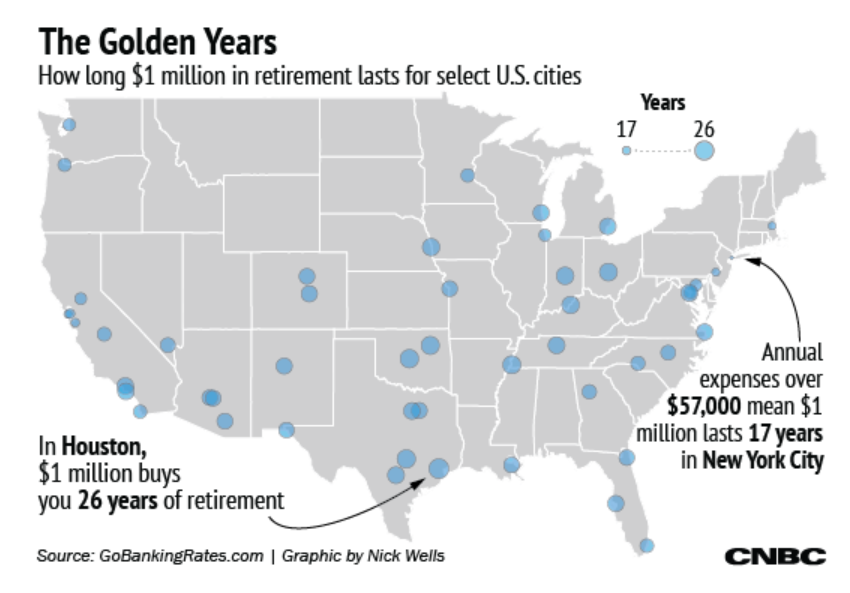

/It’s easy to get swept away with the tides of change and the sensationalized themes that media tends to push forward. Don’t forget, the media needs ratings, conferences and awards to stay relevant and appear “in the know”. How many “industry maps” do you see from companies seeking to outline all the VC’s backed disruption? But here is the staunch reality for wealth management; despite the many innovations and focus on self-directed/digital wealth management – people still lack the ability to retire and robo advisor market share penetration is awfully lacking. A great statement to consider is that $1MM doesn't last as long as it use to, especially considering where you live.

1. Lowest savings rate (2.4% in 2017). We just aren't seeing American's saving more and the odds for retirement are increasingly difficult. This will put pressure on yield adjusted returns for every amount of risk taken - basically, people will adamantly seek yield. Personally, I'm a big supporter of structured products, but that's another story.

2. Cost of living increases in major cities while median income remains stagnant (average hourly wage growth adjusted for inflation has been weak).

3. $1MM doesn’t go far as it use to, especially with the generational wealth transfers that's happening. Most broker dealers are grappling with inheritance related issues - aka the son/daughter blames the broker for putting their parents in financial products that are not suitable. For wealth management firms, this also remains true where you have sons/daughters that complain about the efficacy of their wealth managers. There is a sense of "my turn to lead my financial life" that puts many would-be advisers and brokers at risk. There needs to be more value and relationship investment made in following generation.

At the same time, RIA’s are contending with:

1. Fee pressure - wealth management firms are facing increased scrutiny (from generational transfer of wealth issues to SEC related issues). With Robo's offering a seemingly appealing alternative to provide a digital solution, independent firms will naturally be forces to consider ways to exemplify/communicate and showcase their value proposition at each touch point.

Consideration: perhaps wealth management firms might consider other ways to provide added value (beyond financial planning), and thus increase fees in a down trending environment?

2. Reverse Churning - SEC and FINRA focus regarding this topic. Naturally, the focus will be on brokers switching clients to fee based accounts. However the flip side of this coin is the focus on RIA's - the fee billing history, value add and whether financial advisers have been providing their "fiduciary duty". Regulators will seek evidence of such even though it will come across as insulting from the RIA perspective.

At the same time, we see TAMPs seeking to evolve by using risk adjusted models to sell more solutions and justify their shared basis point existence. It’s not a new thing (quants/hedge funds have been doing this for some time), and from their perspective this is about 5-7 years behind the wealth tech available for the top 1% of the population.

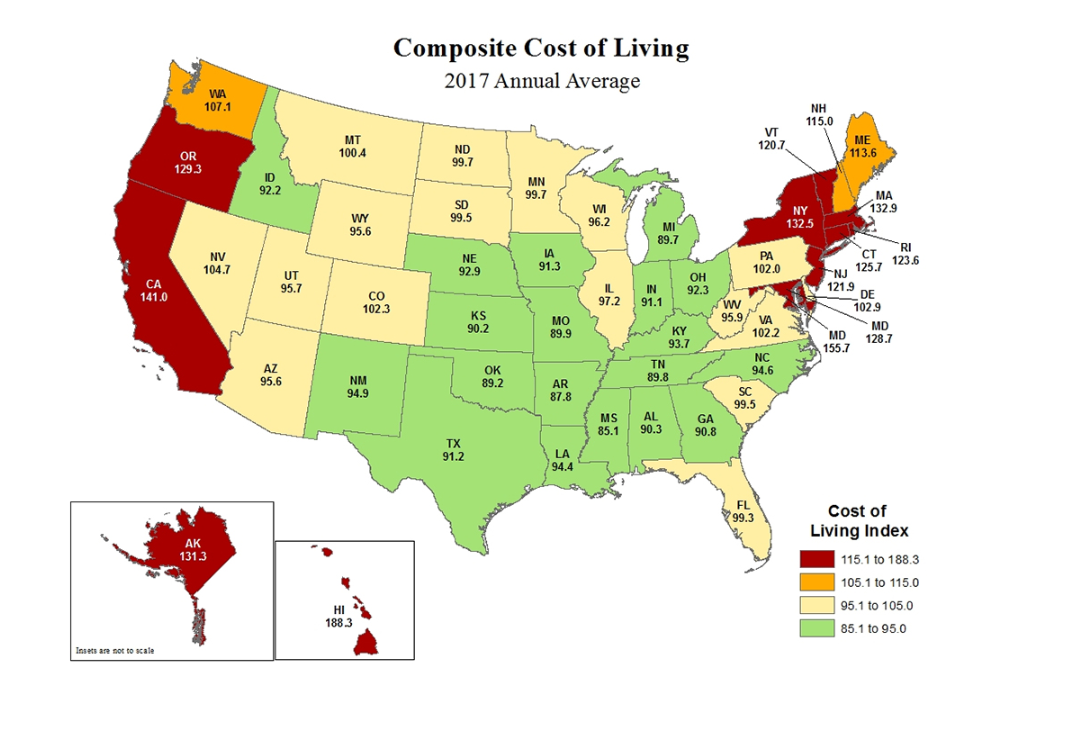

It's from this authors humble opinion that comprehensive models and solutions (especially structured products) must take into consideration a comprehensive view of a client's cost of living (health related costs) and true yield requirements to meet retirement goals. Some fun facts on Cost of Living per state here: